Cracking the Code: Understanding Supply and Demand in Economics Simplified

The concept of supply and demand is the backbone of economics, shaping the prices of goods and services in a market. It's a fundamental principle that affects every aspect of our lives, from the price of the latest gadget to the cost of a simple cup of coffee. In essence, supply and demand dictate the delicate balance between producers and consumers, influencing the fate of entire economies.

Understanding supply and demand can be a daunting task, especially for those new to the field of economics. However, breaking down the concept into its core components can make it more accessible and easier to grasp. In this article, we'll explore the intricacies of supply and demand, providing a simplified explanation of how markets move and prices are determined.

The Law of Supply

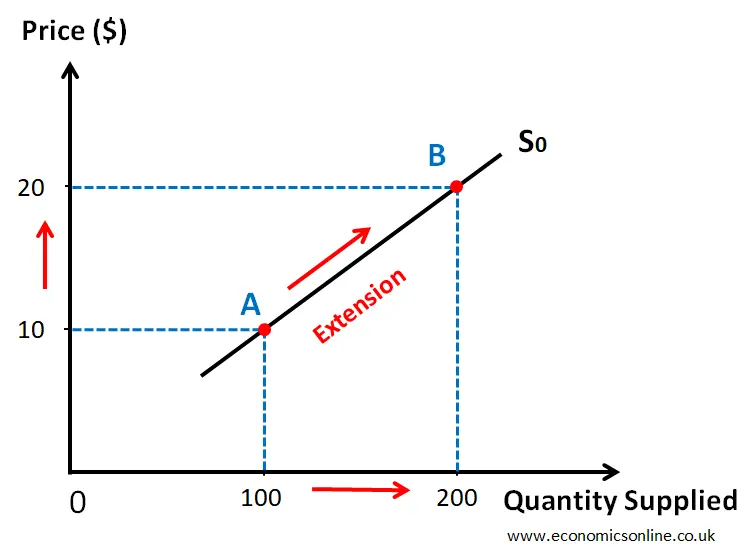

The law of supply, first introduced by Alfred Marshall in 1890, states that as the price of a good increases, the quantity of the good that suppliers are willing to sell also increases. This is because higher prices incentivize producers to supply more of a product, as they can earn a higher profit margin. Conversely, if the price of a good decreases, the quantity supplied will decrease, as producers are not as motivated to supply as much of the product.

"The law of supply is quite simple: if you offer more money for something, people are more likely to do more of it," explains Dr. Rachel E. York, an economist at the University of Texas at Austin. "It's a basic economic principle that's been observed in multiple markets, from commodities to labor."

Here are some key takeaways from the law of supply:

• **Supply increases with price increases**: As the price of a good increases, suppliers are more likely to supply more of the product.

• **Supply decreases with price decreases**: As the price of a good decreases, suppliers are less likely to supply as much of the product.

• **Time and costs influence supply**: Producers' ability and willingness to supply a product are influenced by factors such as time, resources, and production costs.

The Law of Demand

The law of demand, also developed by Alfred Marshall, states that as the price of a good increases, the quantity of the good that consumers are willing to buy decreases. Conversely, if the price of a good decreases, the quantity demanded will increase, as consumers are more likely to purchase the product at a lower price.

"Economists often overlook the law of demand, but it's just as important as the law of supply," says Dr. Brian Greenlee, a microeconomist at the University of California, Berkeley. "It's the driving force behind consumer behavior, influencing what we buy, how much we buy, and how often we buy."

Here are some key takeaways from the law of demand:

• **Demand decreases with price increases**: As the price of a good increases, consumers are less likely to buy as much of the product.

• **Demand increases with price decreases**: As the price of a good decreases, consumers are more likely to buy more of the product.

• **Income and preferences influence demand**: Consumers' ability and willingness to purchase a product are influenced by factors such as income, preferences, and cultural values.

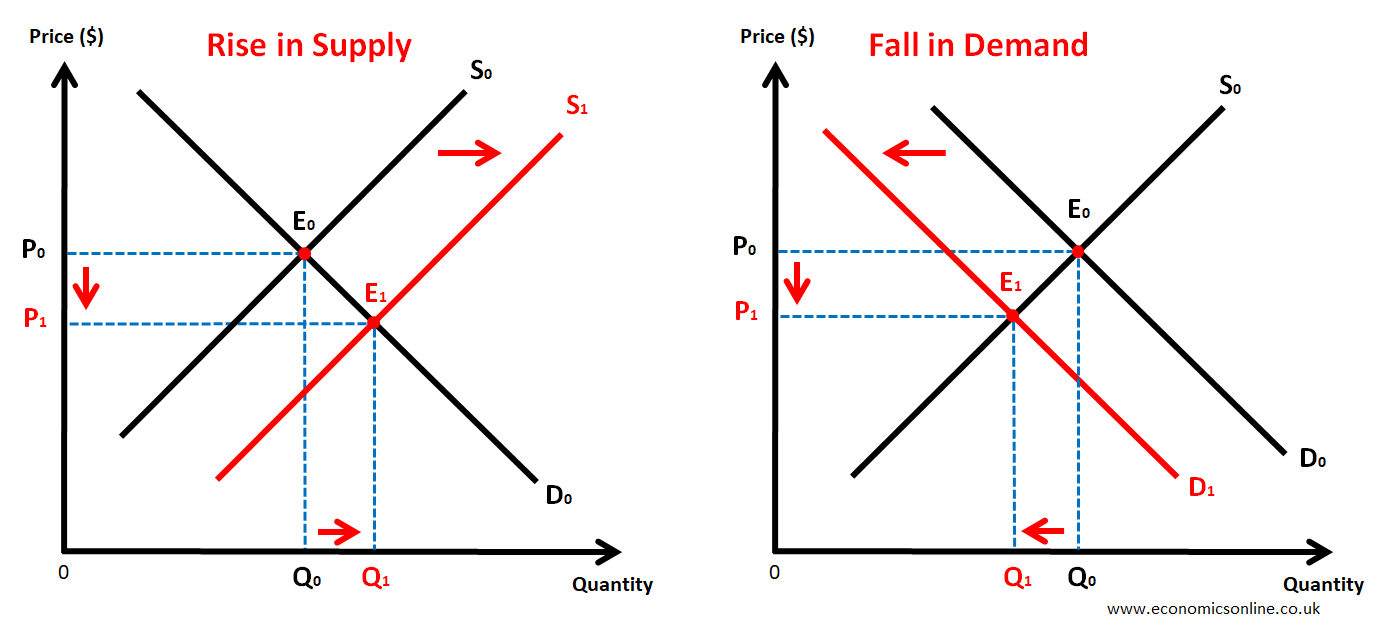

Equilibrium: Where Supply Meets Demand

When the supply curve and the demand curve intersect, the market reaches equilibrium, where the quantity supplied equals the quantity demanded. At this point, the price is stable, and neither the suppliers nor the consumers have any incentive to change their behavior.

"The equilibrium represents the balance between the two key forces of supply and demand," says Dr. Emily Patel, a microeconomist at Stanford University. "It's where the market reaches a stable state, where all parties are content with the current price and quantity traded."

In a perfectly competitive market, equilibrium occurs where the supply and demand curves intersect:

* **Price = Qd = Qs**: The price is equal to the quantity demanded and the quantity supplied.

* **Qd = Qs**: The quantity demanded is equal to the quantity supplied.

Here are some market scenarios where equilibrium occurs:

• **Price ceiling:** When the government imposes a price ceiling (maximum price), equilibrium occurs at the price ceiling.

• **Price floor:** When the government imposes a price floor (minimum price), equilibrium occurs at the price floor.

• **External shocks:** External factors, such as changes in government policies, technological advancements, or global events, can lead to shifts in supply or demand curves, causing a new equilibrium to be reached.

Real-World Applications

Understanding supply and demand has far-reaching implications for individuals, businesses, and policymakers. Here are some real-world scenarios where the concept is essential:

• **Pricing strategy:** Businesses use supply and demand analysis to determine the optimal price for their products, balancing revenue maximization with market conditions.

• **Market forecasting:** Economists use historical data and forecasting techniques to predict supply and demand trends, helping forecast future market prices and revenue.

• **Policy-making:** Governments use supply and demand analysis to inform policy decisions on taxation, subsidies, and regulations, balancing the needs of producers and consumers.

The laws of supply and demand are fundamental to economics, governing the interactions between producers and consumers. By grasping the intricacies of supply and demand, individuals can better navigate markets, businesses can optimize their pricing strategies, and policymakers can create informed decisions that benefit consumers and producers alike. Whether you're a seasoned economist or a curious learner, understanding supply and demand is a crucial step toward mastering the complexities of the economic world.